X-trader NEWS

Open your markets potential

Hong Kong's digital assets: stablecoins, RWA, and digital RMB multi-channel competition

# Hong Kong Advances Multiple Digital Currency Trials: Stablecoins, RMB Digital Currency, and RWA

**Source**: *Caijing* Magazine

**Author**: Kang Kai, *Caijing* Reporter

**Editor**: Yuan Man

**Article Source**: Caijing.com

Hong Kong is simultaneously advancing multiple digital currency trials, including stablecoins, RMB digital currency, and Real World Assets (RWA). With a century-old legacy in finance, Hong Kong now stands at a strategic threshold to embrace the future "carnival of the digital world".

On Hong Kong’s streets, signs for "Octopus" and "Token" are often printed side by side on both sides of the road. This vividly depicts the landscape of Hong Kong’s financial industry: on one side is the century-old accumulation of traditional finance, and on the other is the upcoming "carnival of the digital world".

Today, the integration of traditional finance and the digital world is accelerating. As a bridge connecting the offline and online realms, stablecoins have been entrusted with high expectations by the market. Following the entry into force of the *Stablecoin Ordinance*, the Hong Kong Monetary Authority (HKMA) announced that applications for Hong Kong’s first batch of stablecoin issuer licenses would open from August 1 to September 30, 2025.

Currently, many companies are eager to participate. An HKMA spokesperson revealed that as of August 31, a total of 77 expressions of intent to apply for stablecoin licenses had been received. These institutions include banks, technology enterprises, securities/asset management/investment companies, e-commerce platforms, payment institutions, and startup/Web3 firms.

However, in contrast to the market’s growing enthusiasm, Hong Kong’s regulatory authorities have repeatedly "cooled down" the hype around stablecoins. On August 14, the Securities and Futures Commission (SFC) and the HKMA issued a joint statement emphasizing the need for investors to remain vigilant. The HKMA further stated that only a small number of stablecoin issuer licenses would be granted initially.

In the view of market insiders, this may reflect Hong Kong’s real stance in competing for a share of the digital asset sector. On one hand, it is rapidly advancing the legislative agenda for stablecoins, demonstrating determination to keep up with—even lead—the global trend. On the other hand, to ensure safety, tightening regulation may increase innovation costs for early movers.

In an interview with *Caijing*, Qiu Dagen, a Member of the Legislative Council of the Hong Kong Special Administrative Region, stated that although Hong Kong’s regulation of stablecoins is becoming stricter, this may actually promote industry development. "Stricter regulation will protect the rights and interests of market participants, attract more people to join, and expand the market scale," he explained.

Beyond stablecoins, Hong Kong is also conducting other digital currency trials. The other two initiatives are the "Digital Currency Bridge" project co-led by the HKMA and central banks of other economies, and tokenized deposits issued by banks.

Many market insiders note that these efforts reflect Hong Kong’s diverse attempts in the digital world, but they may also form a "co-opetition pattern" to a certain extent. Both the central bank digital currency (CBDC) bridge project and the commercial application of stablecoins mainly focus on cross-border payments. To build a more efficient cross-border payment system, the two sides need to collaborate in areas such as large- and medium-value clearing/settlement and retail payment in the future.

Market expectations for stablecoin functions extend beyond cross-border payments. By combining the stability of fiat currencies with the efficiency of blockchain, stablecoins may facilitate the development of RWA tokenization—i.e., putting real-world currencies ("money") on the blockchain to invest in virtual assets.

This holds great significance for Hong Kong. In an interview with *Caijing*, Li Ming—Associate Researcher at the AIoT Institute of the Hong Kong Polytechnic University, Chairman of the Blockchain and Distributed Ledger Standardization Committee of the IEEE Computer Society, and Executive President of the Hong Kong Web3.0 Standardization Association—stated that developing the RWA industry in Hong Kong could drive the "going global" of assets from Mainland China while attracting overseas capital inflows. "In the digital world, Hong Kong can still play the role of a ‘super connector’," he said.

At the same time, as the world’s largest offshore RMB hub, Hong Kong can regain vitality in the digital world. If Hong Kong’s stablecoins are pegged to offshore RMB in the future, the growing market scale of stablecoins will promote the internationalization of the RMB.

In this regard, Xiao Feng, Chairman and CEO of Hong Kong-based HashKey Group, told *Caijing*: "Whether in traditional finance or the digital world, to advance RMB internationalization, the key is to expand offshore RMB assets and develop supporting innovative products. Only in this way can we attract overseas investors on a larger scale."

From the perspective of the global monetary system, Li Ming believes that Hong Kong’s stablecoin trials mainly start with application scenarios and focus on innovation in digital finance. In contrast, the U.S. government’s proposed U.S. dollar stablecoins—pegged to the U.S. dollar and U.S. Treasuries—aim to maintain the U.S. dollar’s dominance in the digital world. "To make Hong Kong’s stablecoins widely accepted globally, more efforts are needed in standardization (for technology systems, application scenarios, and industrial ecology), as well as in the design of financial systems and monetary policies," he noted.

# Stablecoins on the Rise: The Tug-of-War Between Innovation and Security

(Photo by Kang Kai: Hong Kong is experimenting with various digital currency payment methods)

“Half seawater, half flame.” – In the eyes of many industry practitioners, this vividly describes the current state of Hong Kong’s digital asset sector: on one hand, it is rapidly advancing the legislative agenda for stablecoins, demonstrating a determination to keep pace with global trends and even take the lead; on the other hand, tightening regulations may increase the innovation costs for early adopters.

After sparking a stablecoin boom, Hong Kong’s financial regulators have recently moved to cool down the enthusiasm. On August 14, the Securities and Futures Commission (SFC) and the Hong Kong Monetary Authority (HKMA) jointly issued a statement on market volatility related to stablecoins, emphasizing the need for vigilance amid market frenzy.

Moreover, Hong Kong’s regulators are raising the threshold for stablecoin approval. HKMA Chief Executive Eddie Yue has repeatedly stressed that the approval criteria for stablecoin issuer licenses in Hong Kong are extremely high, and only a small number of licenses will be granted initially.

The HKMA regards KYC (Know Your Customer) and AML (Anti-Money Laundering) as key priorities for the rollout of stablecoins. According to relevant regulations, the identity information of all stablecoin holders must be retained for more than 5 years. Issuers are not only required to verify user identities but also prohibited from providing services to anonymous wallets.

This move, however, has caused an uproar in the Web3 community. The advantage of decentralized finance lies in its permissionless nature – “open a wallet and use it immediately” – but the real-name requirement essentially transforms stablecoins into regulated digital tools, conflicting with the free circulation characteristics of on-chain native assets.

Some companies even argue that stricter regulations may make it harder for fintech firms to apply for stablecoin licenses, as fintech companies have less experience in implementing KYC compared to financial institutions.

Nevertheless, many market insiders believe that relatively rigorous regulation is more conducive to market development in the early stages of the industry. “Regulations such as KYC and AML set the bottom line for stablecoin policies; what truly determines the market’s upper limit is the implementation of stablecoin application scenarios,” said Li Ming.

Qiu Dagen also holds the view that stricter regulation will protect the rights and interests of market participants and attract more people to join. “Currently, the most important thing for the stablecoin market is to attract enough users. The issuance and circulation volume of stablecoins are not determined by issuers but by demand – stablecoins that are issued but not used must be destroyed. At present, Hong Kong’s regulators have provided clear supervision and tracking processes, allowing people to understand the issuance volume of stablecoins and the bank account status of users.”

Beyond KYC and AML, Martin Rogers, Head of Asia Litigation and Asia Chair at Davis Polk & Wardwell, told *Caijing* that Hong Kong’s regulators are also focusing on financial, credit, and data risks. If a stablecoin issuer defaults, these regulations can protect investors’ rights. Additionally, the use of stablecoins involves uploading large amounts of data to the blockchain, and strict cybersecurity requirements can prevent system hacking.

“Compared with the United States, Hong Kong has more requirements in its stablecoin legislation. The U.S. focuses on information disclosure by stablecoin issuers; on the basis of sufficient disclosure, investors bear risks on their own. In contrast, Hong Kong’s regulators have more provisions to protect investors’ rights,” he further explained.

Even with tighter regulation, many institutions remain eager to enter the stablecoin space. On August 8, Anchorpoint Financial Limited – a joint venture formed by Standard Chartered Bank (Hong Kong), Animoca Brands, and HKT, and one of the three participants in Hong Kong’s stablecoin sandbox – announced that it had informed the HKMA of its intention to apply for a stablecoin issuer license. Liu Yu, CEO of Circle Technology, told Hong Kong’s *Ming Pao* that the company is confident of successfully obtaining the license.

As of August 31, a total of 77 expressions of intent to apply for stablecoin licenses had been submitted to the HKMA. These institutions include banks, technology enterprises, securities/asset management/investment companies, e-commerce platforms, payment institutions, and startup/Web3 firms.

Numerous financial institutions are reluctant to miss out on development opportunities in the digital world. A Hong Kong banking industry insider told *Caijing* that cross-border payments are seen as the most feasible application scenario for stablecoins, and banks have advantages in clearing and settlement services. Most Hong Kong banks are trade banks, and their market networks overlap with the “Belt and Road” initiative – another key advantage. “For some small and medium-sized banks, technological transformation even provides an opportunity to overtake larger competitors,” he said.

From the perspective of fintech companies, Li Ming believes that for enterprises with complex global supply chains, blockchain-based stablecoins can help suppliers receive payments faster. Stablecoin financing based on on-chain trade data is more convenient and cost-effective. At the same time, this can enhance supply chain transparency and trust, and optimize the supply chain ecosystem within enterprises.

In addition, commodities are also regarded as an important application scenario for stablecoins. Qiu Dagen pointed out that commodity trading volumes are large and involve global markets, creating a natural demand for cross-border payment and settlement.

The new energy sector can also provide application scenarios for stablecoins. Tang Bo, Assistant Dean of the Institute of Finance at the Hong Kong University of Science and Technology, told *Caijing* that from a segmented perspective, sectors such as batteries and automobiles have long supply chains, and Chinese enterprises have certain comparative advantages globally. In the future, this will also bring many business opportunities to the cross-border payment field.

Against this backdrop, the market is optimistic about the future prospects of stablecoins. JPMorgan predicts that the stablecoin market size may reach $500 billion to $750 billion in the next few years.

# Digital Currency Co-opetition: Jointly Building a Cross-Border Payment System

Beyond stablecoins, Hong Kong is also conducting various digital currency trials. One is the Central Bank Digital Currency (CBDC) project led by the HKMA, and the other is tokenized deposits issued by banks.

Specifically, Hong Kong’s CBDC exploration can be divided into two categories. At the wholesale level, the HKMA, together with the Digital Currency Institute of the People’s Bank of China, the Bank of Thailand, and the Bank for International Settlements (BIS) Innovation Hub, jointly launched the m-CBDC Bridge project, which is mainly used for cross-border payments and settlements. In addition, the HKMA has also developed “Ensemble” – a wholesale CBDC initiative that builds a new financial infrastructure for cross-bank interbank settlements of tokenized deposits, digital Hong Kong dollars, and regulated stablecoins.

At the retail level, the HKMA has also collaborated with the BIS Innovation Hub and the Bank of Israel to launch the Aurum and Sela projects. These aim to study high-level technical designs for retail CBDCs and test the feasibility of retail CBDC architectures in facilitating digital payments among intermediaries.

Since both the m-CBDC Bridge and stablecoins are mainly applied to cross-border payments in commercial scenarios, many market insiders believe that the two represent the “sovereign path” and “market path” of currency respectively, and may form a distinct “co-opetition pattern.”

However, in Li Ming’s view, the two still have significant complementarity. The m-CBDC Bridge serves large- and medium-value clearing and settlement at the wholesale level, such as reserve transfers between central banks and cross-border settlements of national-level commodities. Stablecoins can accelerate high-frequency demand at the retail level, such as small-value payments or financial services between commercial institutions. As stablecoins gradually become compliant and the application scenarios of the m-CBDC Bridge expand, the two can jointly form a more efficient cross-border payment system.

Tang Bo believes that the m-CBDC Bridge, based on the CBDC framework, emphasizes regulatory compliance and financial stability. While this reduces systemic risks, it lacks flexibility. Stablecoins, on the other hand, are built on public blockchains, smart contracts, and an open financial ecosystem, making them more suitable for high-frequency, fragmented payment scenarios.

In terms of tokenized deposits, HSBC is a pioneer. In May, the bank announced the launch of a corporate treasury management solution focused on tokenized deposits in Hong Kong – the first blockchain-based settlement service provided by a bank in Hong Kong. Initially, its corporate clients can transfer and pay Hong Kong dollars or U.S. dollars between wallets held by different companies under their names. The process is not restricted by trading hours and can be completed in real time, helping enterprises improve treasury management efficiency.

Ant International became the first corporate client to adopt this solution. After tokenizing the deposits in its HSBC account, the company successfully completed real-time internal fund transfers.

McKinsey believes that all three types of trials can improve the efficiency of settlement and payment. Thanks to technologies such as digital compliance processes and smart contracts, regulators can address AML and KYC issues through on-chain analysis services.

However, McKinsey notes that these trials may pose a direct challenge to global payment systems such as Swift. If current growth rates continue, stablecoin transaction volumes may surpass traditional payments in less than a decade. To date, traditional payment infrastructure handles $5 trillion to $7 trillion in global remittances daily (including those from financial institutions, enterprises, and individual consumers).

Zhang Tao, former Chief Representative of the BIS Asia-Pacific Office, told *Caijing* that the global payment system is in a continuous process of improvement. Any improvement to this system should, on the basis of legality and compliance, strive to provide better services to consumers at the lowest cost. “In other words, it is about enabling consumers to transfer money from one place to another in a cheaper, faster, more stable, secure, and compliant manner. Current technological advancements have created more possibilities for enhancing and improving the global payment system,” he said.

“For cross-border payments, whether using CBDCs or stablecoins, the underlying blockchain technology is relatively mature. Next, the focus of all parties is how to implement their application scenarios. What matters is to better integrate financial services with blockchain-based digital finance and innovate businesses in the direction of improving efficiency and increasing transparency,” Li Ming said.

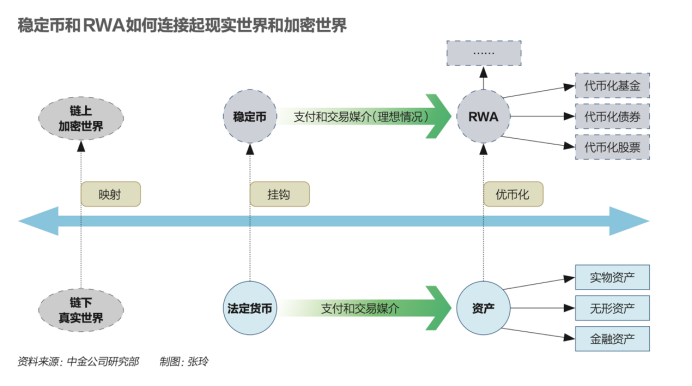

# RWA: The Next Frontier for Virtual Assets

Beyond cross-border payments, market insiders have even greater expectations for the functions of stablecoins. In their view, by combining the stability of fiat currencies with the efficiency of blockchain, stablecoins may facilitate the development of Real World Assets (RWA) tokenization.

RWA refers to the process of tokenizing real-world assets using blockchain technology, enabling them to be traded in the cryptocurrency market or used as collateral.

From the perspective that all real-world assets can be mapped onto the blockchain, fiat-backed stablecoins are the most basic type of RWA – essentially putting real-world currency (“money”) on the blockchain. Compared with other RWAs, the underlying assets of fiat-backed stablecoins are the most fundamental and liquid form of assets (i.e., money). Stablecoins serve as the basic medium for RWAs, and other RWAs (“assets”) can use stablecoins as a trading medium.

Take Hong Kong as an example: RWA projects can use stablecoins pegged to the Hong Kong dollar or U.S. dollar as payment or redemption channels to map the value of real estate, bonds, stocks, intellectual property, and even carbon assets onto the blockchain for tokenization, enabling global trading or financing. As the scale of stablecoins continues to expand, the demand for on-chain allocation will grow, thereby promoting the development of RWAs.

Li Ming believes that developing the RWA industry in Hong Kong can leverage China’s advantages in manufacturing and supply chains, drive the “going global” of Mainland China’s assets, and attract overseas capital inflows. “In the digital world, Hong Kong can still play the role of a ‘super connector’,” he said.

Specifically, Hong Kong’s current RWA practices mainly adopt a cross-border RWA tokenization model of “Mainland China assets + consortium chains + Hong Kong regulatory sandboxes,” focusing on four themes: fixed income and investment funds, liquidity management, green and sustainable finance, and trade and supply chain finance. Among the RWA tokenization projects in Hong Kong’s Ensemble sandbox program, three involve Mainland assets: RWA for Longshine Group’s new energy charging piles, RWA for GCL New Energy’s photovoltaic power plants, and RWA for Xuny Eagle Travel’s battery swapping assets. The underlying assets are mainly future income rights from new energy.

Tang Bo believes that the effectiveness of this cycle depends on the availability of high-quality new energy assets for investment. For example, many new energy enterprises are currently building photovoltaic and wind power facilities overseas. If investors can obtain substantial cash flow returns by purchasing these assets in the RWA space, they will naturally be willing to hold the corresponding stablecoins. This is equivalent to using stablecoins for cross-border energy trade and then investing in new energy RWA assets.

Qiu Dagen also notes that investors hold stablecoins mostly to access the underlying digital assets. However, he also cautions that stablecoins are just a small piece of the larger digital world puzzle. Behind this, the key is to unlock hard-to-trade assets through tokenization, addressing the lack of liquidity caused by poor tradability.

In this regard, Li Ming believes that the liquidity dilemma of RWAs largely stems from whether the underlying assets can be standardized. “Compared with the U.S., which uses financial assets as the underlying for RWAs, China’s underlying assets are mostly physical assets, which are more difficult to standardize. This actually reflects a fundamental difference: the U.S. is a financial power, while China is a manufacturing and supply chain power. However, if these physical assets can be activated in the virtual world in the future, they can greatly support the ‘Belt and Road’ initiative and the dual-circulation strategy,” he said.

(How Stablecoins and RWAs Connect the Real World and the Crypto World. Chart Source: Research Department of China International Capital Corporation (CICC))

At the same time, as the world’s largest offshore RMB hub, Hong Kong can also thrive in the digital world. If Hong Kong’s stablecoins are pegged to offshore RMB in the future, the growing market scale of such stablecoins will drive the internationalization of the RMB.

From Qiu Dagen’s perspective, from the standpoint of Hong Kong’s regulatory authorities, offshore RMB is one of the options for Hong Kong’s stablecoins to be pegged to fiat currency. “Currently, the volume of cross-border RMB payments and settlements is gradually increasing, which serves as a crucial entry point for the development of offshore RMB stablecoins. To make transactors willing to hold offshore RMB stablecoins, holders need to have more RMB investment channels. For instance, holders can deposit RMB in banks to earn high interest, or invest in financial assets such as stocks and bonds. This process is aligned with the internationalization of the RMB itself,” he said.

Data from the People’s Bank of China (PBOC) shows that in 2024, the cross-border RMB receipt and payment volume reached approximately RMB 64 trillion, a year-on-year increase of 23%. Up to now, offshore RMB payments processed through Hong Kong have consistently accounted for over 70% of the global total. Hong Kong has the largest RMB liquidity pool outside Mainland China, with a scale of roughly RMB 1 trillion.

Xiao Feng believes that Hong Kong is a crucial “bridgehead” for advancing the internationalization of the RMB—whether in the current financial market or the future digital world. At present, countries and regions such as the United States are promoting tokens; if Hong Kong, China does not make such attempts, it may struggle to integrate into the digital world in the future. From the perspective of promoting offshore RMB stablecoins, China accounts for a large share of global trade in both exports and imports. How to integrate trade settlements with stablecoins may become a key driver for advancing this process.

From the perspective of the global monetary system, Li Ming believes that Hong Kong, China still has a long way to go in promoting stablecoins in the future. By comparison, the U.S. government’s proposed U.S. dollar stablecoins are pegged to the U.S. dollar and U.S. Treasuries, aiming to further strengthen the U.S. dollar’s dominance in the digital world. In contrast, the stablecoins promoted by Hong Kong, China mainly start with application scenarios, with the greater goal of driving the development of the digital economy through financial innovation. To gain widespread global acceptance, more efforts are needed in terms of standardization, industrial policies, and monetary system design.

Disclaimer: The views in this article only represent the author’s personal opinions and do not constitute investment advice for this platform. This platform makes no guarantees regarding the accuracy, completeness, originality, or timeliness of the information in the article, nor does it assume any responsibility for losses arising from the use of or reliance on the information in the article.

Contact: Sarah

Phone: +1 6269975768

Tel: +1 6269975768

Email: xttrader777@gmail.com

Add: 250 Consumers Rd, Toronto, ON M2J 4V6, Canada

+1 6269975768

+1 6269975768 微信

微信 Teams

Teams